White Paper

Pandemic-Driven Medicaid and ACA Expansion

Summary

Learn more about expected changes in the composition of national Medicaid and ACA member populations, and the potential financial consequences of the pandemic.

White Paper | Jimmy Liu

Vice President of Risk Analytics, Change Healthcare

Vice President of Risk Analytics at Change Healthcare, is responsible for supporting the company’s Medicare, Medicaid, and Commercial ACA lines of business, with a focus on analytics, strategy, and innovation. He was one of the original developers of the Risk ViewTM application, which helps plans receive appropriate payment based on the relative health of the at-risk population. As an expert in risk adjustment and risk scoring models, Jimmy has been helping health plans better understand and formulate their risk adjustment strategy for the past 10 years.

Whitepaper | Dan O' Brien

Director for Risk Adjustment Strategy, Change Healthcare

Dan O’Brien is the Director for Risk Adjustment Strategy at Change Healthcare. Dan has worked in healthcare for more than 25 years, and has spent 15 years within health plans running a combination of Medicare Advantage, Medicaid, and ACA Exchange lines of businesses. His expertise includes health plan finance and operations, revenue optimization, medical expense initiatives, strategic planning, federal and state relations, risk adjustment/encounter submission, vendor management, provider contracting, and value-based arrangements.

Executive Summary

Understanding the full impact of the COVID-19 pandemic on the healthcare industry is not yet possible, but a few outcomes are evident. Medicaid and Affordable Care Act (ACA) enrollment rates are surging alongside the unemployment rate.1 In addition, postponed procedures and delayed routine services—as well as pent-up demand for elective procedures—will soon drive increased utilization.

This report details expected changes in the composition of national Medicaid and ACA member populations, and explores the potential financial consequences of the pandemic on payers. We address the timing of the Medicaid/ACA expansion and provide five immediate, actionable strategies to help payers mitigate challenges caused by the pandemic:

- Prepare your infrastructure by expanding provider networks to increase capacity; expect and plan for payment delays from financially unstable states.

- Collaborate with providers to ensure that members who are most at-risk receive access to necessary healthcare services.

- Accurately identify primary healthcare insurance coverage to reduce exposure and avoid costly recoveries.

- Identify and capture missing risk-adjusting diagnostic codesfor members by year’s end, using technology to close risk gaps and validate claims before submission.

- Aggressively manage risk scoresby identifying members in need of documentation and proactively facilitating care visits by the end of the calendar year.

To ensure financial stability amid the new pandemic environment, payers should prepare to address shifting capacity, care accessibility, and utilization rates while managing a greater percentage of Medicaid and ACA members.

Introduction

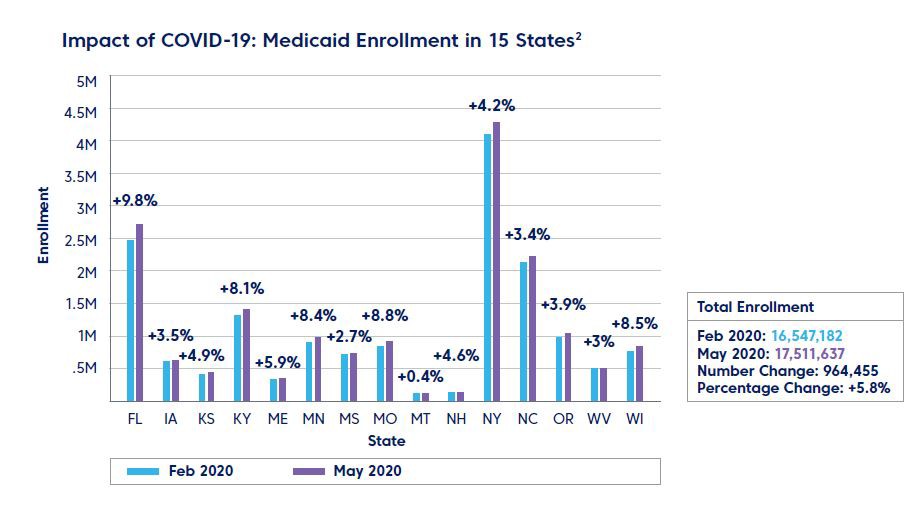

As a result of the COVID-19 pandemic, unemployment rates have skyrocketed across the country, driving a massive expansion in Medicaid and ACA enrollment.

As the economy rebounds, coverage will likely shift back to commercial lines of business and payers should be prepared for continual changes in coverage for the foreseeable future. Maintaining accurate eligibility information about this fluctuating population will be a challenge for payers. Further, payers will continue to experience the impact of this migration on their bottom line. New Medicaid members will be healthier than the traditional Medicaid population, but will drive higher utilization rates at lower margins.

In addition, pandemic-related interruptions to the care delivery process may make it difficult for payers to fully implement their typical risk adjustment strategies by year’s end. A new risk management strategy is necessary to minimize losses and position payers for long-term success in this new environment.

The New Face of Medicaid

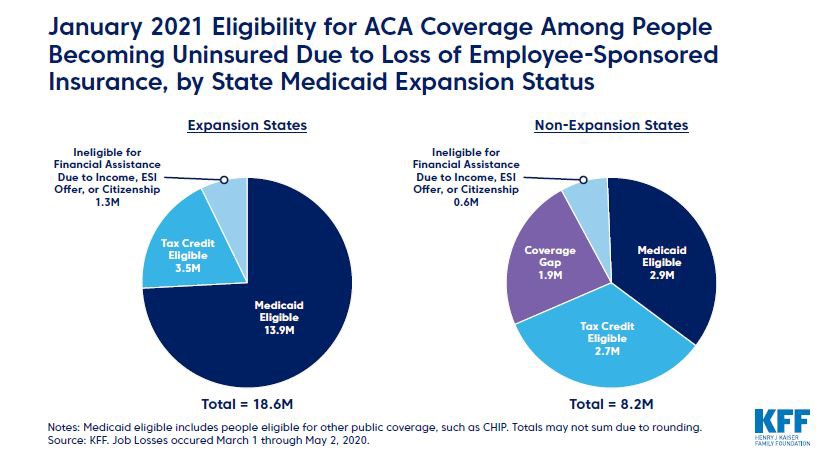

As people lose their jobs and become ineligible for employer-sponsored insurance (ESI), they are seeking new coverage from governmentsponsored plans. Of those losing coverage, nearly half are eligible for Medicaid, and an additional 31% are eligible for marketplace subsidies.3

Because many newly eligible Medicaid and ACA enrollees are predominately transitioning from ESI plans, the influx as a whole will be more similar to typical ESI and ACA populations than to traditional Medicaid populations—more financially stable, educated, and healthier.4

Although this healthier population will likely spend less on healthcare services, payers should keep in mind two factors that might drive up healthcare utilization for certain procedures: delayed demand and expanded benefits. Many services, such as dental and vision, are covered in full under Medicaid. New enrollees who have never received such benefits might opt to complete free elective procedures while they have time and remain unemployed.

Pent-up demand for necessary healthcare services, coupled with broader coverage, will potentially drive greater utilization. However, initial resource constraints will likely make care accessibility a significant challenge for many patients.

61% of Americans experiencing job loss had ESI, and a vast majority will be eligible for ACA assistance either through Medicaid or subsidized marketplace coverage. This influx as a whole will be more similar to typical ESI and ACA populations than to traditional Medicaid populations—more financially stable, educated, and healthier.5

Longer-Term Impact of Increased Utilization

The timing and financial impact of new Medicaid and ACA enrollees is dependent upon a number of factors, including processing backlogs at state agencies, the overall increase in demand, and the accessibility of healthcare services.

Outdated technology and understaffing are delaying unemployment enrollment, and some individuals have struggled for weeks to obtain benefits.6 A similar backlog for Medicaid enrollment should be expected. Typically, a new member is assigned to a Managed Care Organization (MCO) within 45 days after enrolling.

Current processing backlogs indicate that window will likely expand significantly and it might be 60 to 90 days before members can receive care through an MCO after enrollment—and that is dependent on the availability of healthcare services.7 Many states are attempting to expedite coverage for eligible families by expanding the types of providers who can perform Presumptive Eligibility (PE), potentially reducing the overall timeline.

The demand for healthcare services has also begun to increase, and given the timing and delays described above, is expected to hit a high in the fourth quarter of 2020 and continue into 2021. While many patients will receive healthcare services in 2020, we expect the most dramatic impact of Medicaid member utilization to hit in 2021, when care services are likely to be more widely accessible.8

Geographic Implications

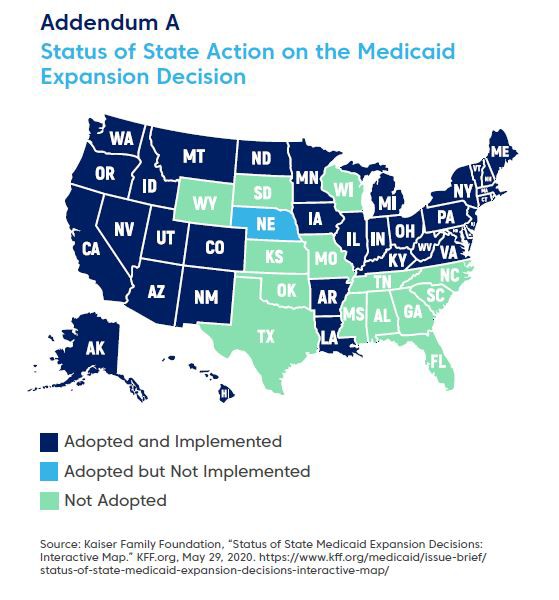

Assuming unemployment extends into 2021 when unemployment insurance (UI) benefits would likely expire, the proportion of people eligible for Medicaid would increase in states with Medicaid expansion, while non-expansion states may see more nonelderly adults moving into the Medicaid coverage gap.9 For a full list of expansion and nonexpansion states, see addendum A*.

Payer profitability will doubtless suffer, as the low utilization rates for a third of 2020 will provide only short-term financial gain. In addition to increased membership in plans that yield lower profits, operational interruptions will make it difficult for payers to implement risk adjustment strategies by the close of the year. Payers must take immediate action to manage these challenges.

We expect the most dramatic impact of Medicaid member utilization to hit in 2021, when care services are likely to be more widely accessible.

Navigating the Pandemic Environment: 5 Strategies for Payers

Based on the insight provided above, the following are strategies to mitigate the impact of this tumultuous environment.

Prepare Organizationally

Payers can help increase utilization by expanding their provider networks to include new points of care, such as minute clinic

Expand Provider Networks

Given the restrictions on elective procedures from March through June, the healthcare system will likely experience exceptionally high care demands in the latter half of 2020, causing bottlenecks in existing provider networks. Payers can help increase utilization by expanding their provider networks to include new points of care, such as minute clinics.

Expanding provider networks will require the use of data analytics to target high-quality, highefficiency providers. We recommend payers identify those providers who have both the capacity and the systems in place to handle high volume at low cost. These insights can inform a payer’s provider network expansion strategy to help ensure that patients in need—especially those with serious and chronic conditions—are seen promptly.

Expect and Prepare for Payment Delays

States grappling with high unemployment rates and reduced revenue might rely upon payment schedule changes to help ameliorate their finances. Payers should explore methods for handling potential payment delays from these states. One consideration to note is that states do have the flexibility to change when they pay Medicaid MCOs. For example, some states may move from prospective payments to retrospective payments, while others might skip the last payment of a fiscal year and push the payment into the next fiscal year. Pennsylvania Medicaid has used this payment schedule several times, for example.

Proper cash flow forecasting will be extremely important during the delayed payment period. We recommend working with your state Medicaid agency and their designated actuarial firm to ensure a proper timetable for plans to be made whole.

Prioritize Members

Months of deferred care will result in a pent-up demand for services, placing a great deal of pressure on providers already operating at reduced capacity. New peaks of COVID-19 patients might continue to overwhelm hospitals, complicating both actual and expected patient flow. To effectively manage risk, payers need to prioritize patients to ensure that those with the highest risk can access care services.

On average, patients visit a physician three times a year.10 In 2020, pandemic-related delays will likely drop that average to two visits per year per patient. One less office visit is one less opportunity for payers to capture a potential diagnosis needed to drive risk scores. Payers will need to be proactive in partnering with providers to capture every possible diagnosis at the remaining office visits. Closing risk gaps by year’s end will be difficult but essential to optimizing profitability in 2021.

Accurately Identify Primary Coverage

Research shows that private insurance matches miss about 7% of individuals with additional coverage.11

Ensuring accurate identification of each member’s primary payer is essential for maximizing cost avoidance—especially during sudden largescale shifts in healthcare coverage. If an enrolled member has multiple sources of healthcare coverage, the primary coverage must be appropriately assigned in order to avoid costly and time-consuming recoveries.

Determining the existence of alternate coverage can be challenging. Research shows that private insurance matches miss about 7% of individuals with additional coverage.11 Considering that an estimated 27 million people became uninsured as of May 2, 202012, 7% represents sizable exposure.

Payers must have ready access to the latest coverage information and the algorithms that ensure accurate data matching the first time around. When mistakes are made, they need to be identified quickly and resolved in a way that minimizes provider abrasion.

Finally, effective coverage identification will help payers prepare for when the economy improves, and the members migrate back to the commercial plans.

Identify Risk-Adjusting Diagnosis Codes

The pandemic compressed healthcare delivery in 2020, leaving providers with a shorter period of time in which to treat patients. This means that there is also a limited window of opportunity to review claims and capture missing chronic diagnosis codes—which is likely to negatively impact risk payments.

Payers need to be aggressive about capturing diagnoses until December 31, 2020, and should apply processes and technology to close risk gaps by the deadline. By using technology that automatically identifies potentially missing codes based on historic claims data, payers can prompt providers to correct claims in real time, before they are submitted. Given the short lead time, payers should look for software that does not require installation and that makes coding validation an integral part of the claims submission process.

Payers should also be proactive in their outreach to targeted, high-risk populations. By sending personalized messaging to members with chronic conditions, payers can prompt those who have not yet been treated to schedule an appointment.

Ramping up chronic care management and care coordination services has a two-fold impact on both patient outcomes and revenue. Maximizing risk score accuracy can have long-term benefits for a payer’s risk adjustment strategy and overall profitability.

Technology that automatically identifies potentially missing codes based on historic claims data, payers can prompt providers to correct claims in real time.

Practice Aggressive Risk Score Management

Risk adjustment performance is critical to the success of a health plan’s government-sponsored insurance business. Although the pandemic is certain to cause a negative impact to payers’ risk scores, immediate intervention could mitigate the effects of delayed care by the end of 2020.

Understanding risk score opportunities will help payers drive financial gains by optimizing targets for appropriate risk-adjusted reimbursement. As some new Medicaid members have not visited a physician all year, they have virtually no risk score on record. Payers will need to act quickly to obtain accurate risk scores for these enrollees.

To reduce the magnitude of the pandemic’s impact, payers should work to resolve gaps in care in their member populations. Payers can proactively identify patients who have not yet had their conditions documented. These members may need to be scheduled for additional physician appointments, or their charts selected for a retrospective chart review. Encouraging members to use telehealth services may help offset missed provider visits, but these virtual encounters may not capture as many risk codes as on-site appointments.

A Look Ahead

As states end their various quarantine phases and open additional businesses and services, the country may experience accompanying spikes in COVID-19 cases—as well as second, third, and fourth waves of restrictions. From an economic perspective, a prolonged pandemic will almost certainly result in increased unemployment, further expansions to Medicaid, and more state budgets facing insolvency.

For payers, the usual way of doing business is no longer applicable. Adjusting to rapidly shifting regional capacity, care accessibility, and utilization rates will require a concerted strategy for managing risk adjustment amid the new market conditions. Planning and preparation are key to succeeding and overcoming these challenges.

1. Robin Rudowitz and Elizabeth Hinton, “Early Look at Medicaid Spending and Enrollment Trends Amid COVID-19.” KFF, Henry J. Kaiser Family Foundation; May 15, 2020. https://www.kff.org/coronavirus-covid-19/issue-brief/early-look-atmedicaid- spending-and-enrollment-trends-amid-covid-19/

2. Joan Alker, “As Expected, Medicaid Enrollment Is Starting to Increase.” Georgetown University Health Policy Institute; May 14, 2020. https://ccf. georgetown.edu/2020/05/14/as-expected-medicaid-enrollment-is-starting-toincrease/

3. Rachel Garfield, Gary Craxton, Anthony Damico, and Larry Levitt, “Eligibility for ACA Health Coverage Following Job Loss.” Kaiser Family Foundation; May 13, 2020. https://www.kff.org/coronavirus-covid-19/issue-brief/eligibility-for-acahealth- coverage-following-job-loss/

4. Ibid.

5. Ibid.

6. Courtenay Brown and Kyle Daly, “Creaky Unemployment Systems Plague Jobless Americans.” Axios; May 1, 2020. https://www.axios.com/creaky-unemploymentsystems- plague-jobless-americans-b5244634-f72b-4b33-a65d-dbc2f0f5492a.html

7. Jennifer Wagner, “Streamlining Medicaid Enrollment During COVID-19 Public Health Emergency.” Center on Budget and Policy Priorities: May 13, 2020 https:// www.cbpp.org/research/health/streamlining-medicaid-enrollment-during-covid- 19-public-health-emergency

8. Garfield et al, “Eligibility for ACA Health Coverage Following Job Loss.”

9. Achilles Natsis, FSA, MAAA, “Impact of COVID-19 on Deferred Medical Costs and Future Pent-Up Demand.” Society of Actuaries: April 2020. https://www.soa.org/resources/research-reports/2020/covid-19-deferred-medical-cost/

10. Jill J. Ashman, Ph.D., Pinyao Rui, M.P.H., Titilayo Okeyode, FSA, MAAA, “Characteristics of Office-based Physician Visits, 2016.” Center for Disease Control and Prevention: January 2019. https://www.cdc.gov/nchs/products/ databriefs/db331.htm#:~:text=During%202016%2C%20the%20overall%20 rate,278%20visits%20per%20100%20persons.

11. Internal Change Healthcare data.

12. Change Healthcare internal statistics based on data for all customers using the Coordination of Benefits solution during a one-year period. Individual results may vary.